Russia Gas Closure Spoils A Goldilocks Job Report

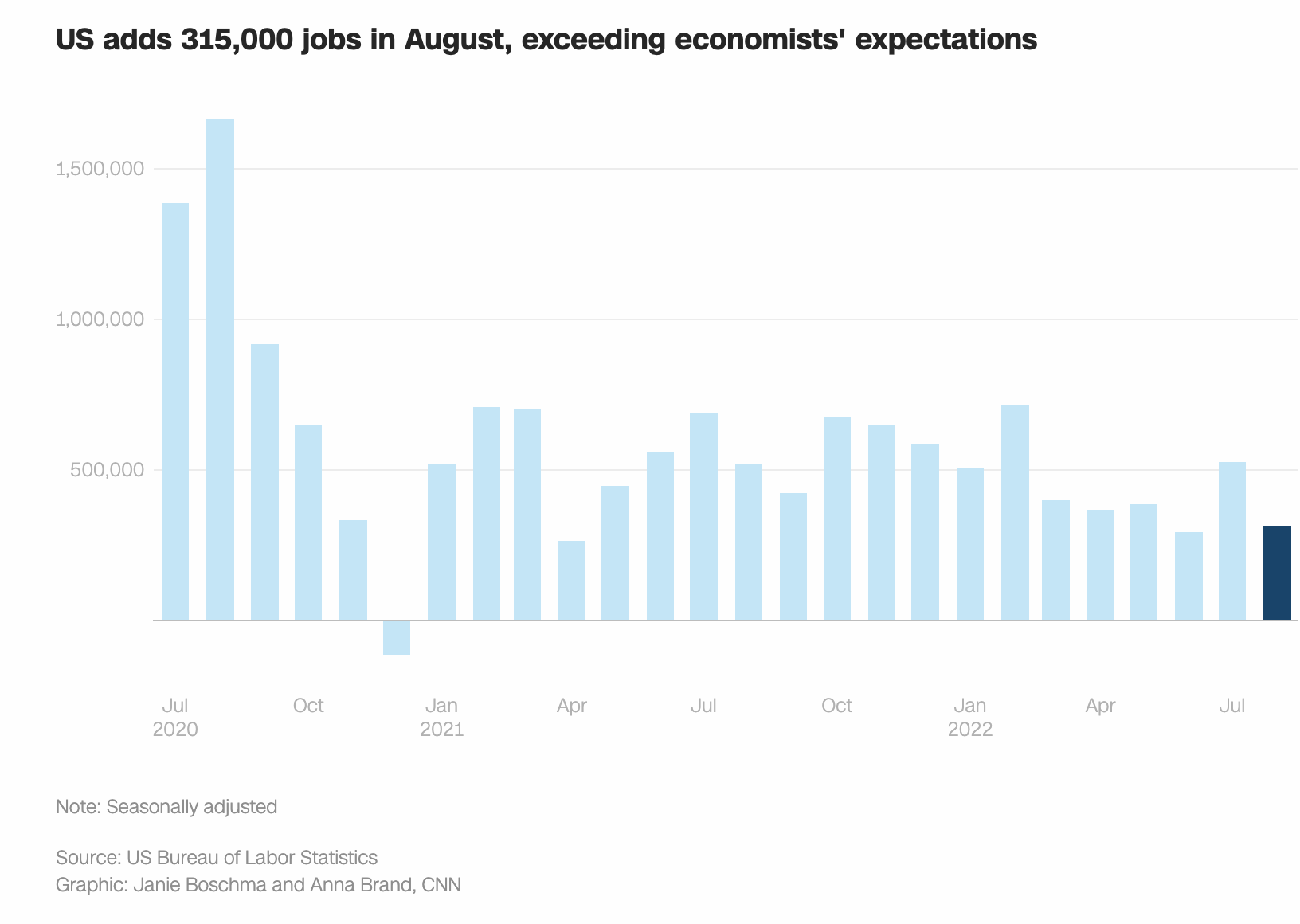

Equity markets were soothed earlier in the day due to an as-expected August Jobs Report. Hourly earning increases fell and more people entered the workforce. This is a sign that inflation is forcing people to accept jobs and re-think life without work. A volatile stock market has pushed older workers back into employment, as retirement accounts have been jeopardized by the traditional 60% stock/40% bond allocation this year. And, just when you thought the equity markets were gaining some footing… Gazprom, the Russian-controlled gas company, shut down its pipeline to Europe citing an oil leak. This news was not unexpected but took equities and U.S. Treasury yields lower. The markets are in some mood. It is virtually impossible to estimate where the U.S. economy, real estate prices, and interest rates are headed. There are simply too many variables to consider and too many black swans circling

Navigating The Gazprom Effect

Taking the Fed at face value, a 50 bp hike is certain. However, one cannot rule out 75 bp, especially if oil starts surging again in response to the Gazprom news. The Baseline Fed Funds rate is gaining support for settling at around 4.00%. Inflation is starting to show signs of moderating, but it is mathematically improbable that it will fall to the Fed’s target rate of 2% in 2023. Wall Street has had to reevaluate the higher interest rates for a longer Fed narrative as the interest rates start to do their job. Meanwhile equity and bond prices have fallen, real estate is under pressure, and business confidence remains between cautious to downright negative. The return to a more normal interest rate environment is resetting asset prices.

I want to say a few words about the manner in which I write this weekly blog. While I am personally inclined to be a little more conservative in my thinking, I do my very best to paint a weekly picture of what I am reading. In addition to the news and other industry sources, everything shared in terms of the economy’s direction is combined with the feedback I receive from our network of clients and bank executives. Lately, the current environment is not too positive. In my opinion, we are already in a recession. That is probably going to get worse before it gets better. However, one must remember it is during times of heightened volatility and turmoil that some of the best investments present themselves. So, while I am not bullish on the economy at the moment, I do believe patience will pay off in the form of lower house prices, and better entry points for non-housing investments.