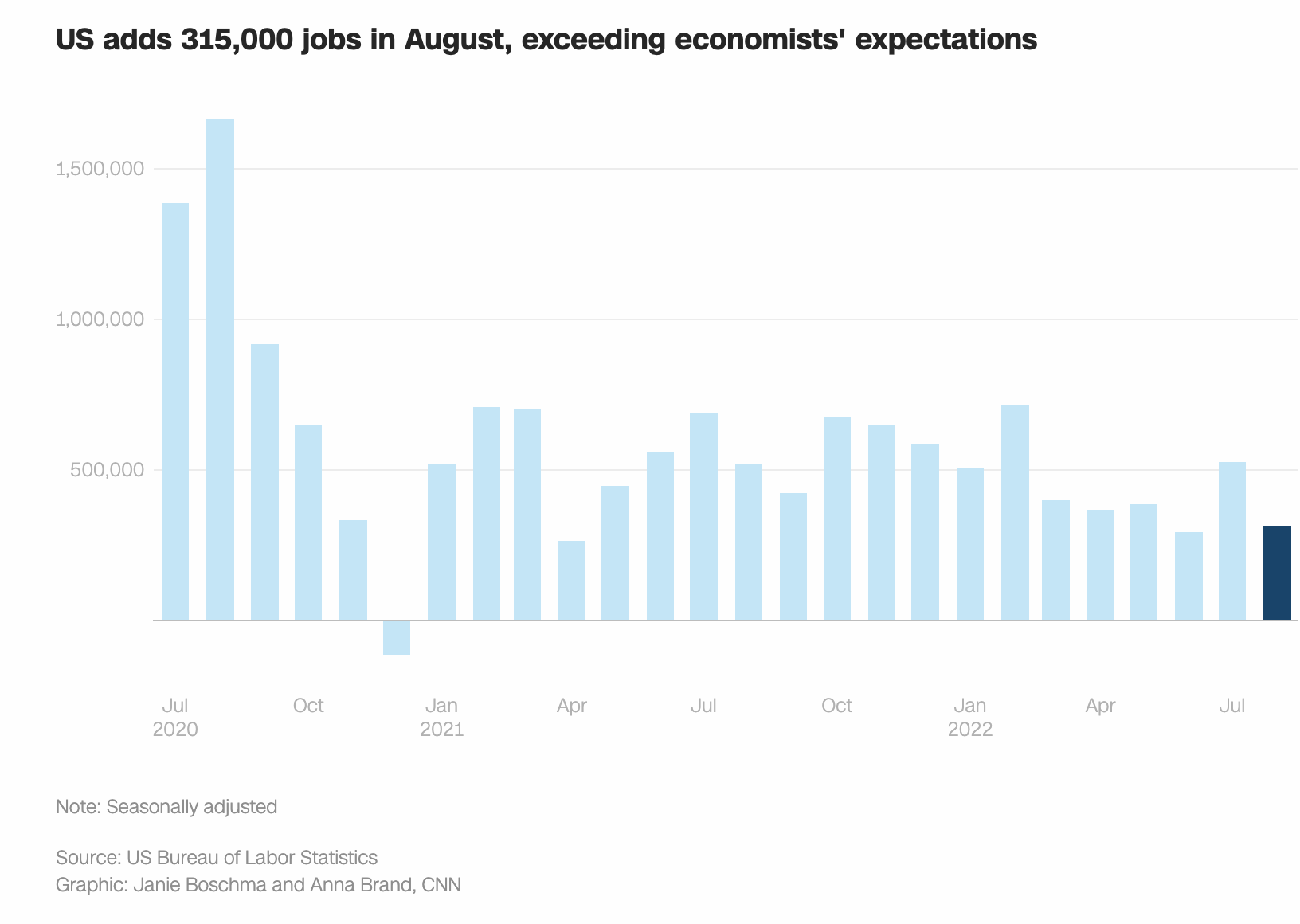

All Eyes On Fed Next Week As Markets Remain On Edge

FedEx, one of the premier delivery companies worldwide, warned of a global recession. This is concerning news, given their intimate knowledge of the manner goods and services flow through the global economy. This warning came on the heels of ongoing fears amongst market participants about inflation, Fed tightening, and stagflation anxiety (stagflation is the combination of rising costs, higher unemployment, and slowing growth). One can look at the equity markets as a proxy for deflating asset prices worldwide. Fed Chair Powell echoed this much when he used the word “pain” on two separate occasions when discussing the Fed’s plans to bring inflation down, which is through the combination of higher rates and wealth destruction. One should remember the words “don’t fight the Fed” applies to both uptrends and downtrends.

How Deep Will The Recession Go?

A .75 bp hike on the short-term Fed Funds Rate is baked in at near 100%. However, there is a chance the Fed may go up to 100 bp in hikes. Given the slowdown in housing, the destruction of wealth in many Americans’ retirements, equity/bond holdings, and the grim outlook by business owners, our hope is that a 100 bp hike does not become a reality. Slow and steady may be a better policy. We have advocated for more and faster hikes in previous commentaries, but, the combination of Fed hikes and quantitative tightening (which is just rolling out) may succeed in bringing down inflation. The aim at this point is to avoid a deep global recession. The comments from FedEx should not go ignored. Next week’s Fed meeting is so important, as a too-aggressive Fed could break something, which would not be good. Breaking inflation by way of an international financial crisis serves no one’s interests and would do more harm than good.

The Lending Narrative Continues

On the lending side, higher short-term rates and even higher longer rates impede the ability of new buyers to qualify for mortgages. Home builders are trading poorly as are home improvement companies. Housing is a major component of GDP growth so there is no doubt in our minds that the U.S. is in a mild recession. The bigger question is, how long does this last? When do interest rates top out, how will new and existing home sales and all other property types adjust to much higher interest rates? While there are lenders making practical decisions on applicants, increased mortgage payments have doubled from where they were just a few months ago. This will be a drag on housing prices, even with the limited demand in many large cities. A bit of positive news though, as potential new buyer income is holding up, and many are looking to the current volatile market as a good entry point.

The great Warren Buffet is famous for saying he is greedy when others are fearful. Well, there is certainly fear in the air. Smart and thoughtful purchases of assets such as real estate or high-quality equities may be at the beginning phase of attractiveness.