A Tale of Two Housing Markets As Rates Rise

Even with the rise in interest rates, the limited supply of existing homes for sale is leading to multiple offers on the more affordable properties entering the market. This growth in demand is a key factor behind the surge in builder stocks reaching near all-time highs. New home construction is crucial as many homeowners are hesitant to sell their homes. This situation also highlights the importance of recognizing that real estate markets cannot be generalized. The ultra-high-end existing and new home market, particularly homes priced over $10 million, is not experiencing the same level of activity due to higher interest rates and concerns about the economy.

Despite potential negative news such as debt ceiling talks and rising interest rates, the stock market remains unfazed, largely driven by the future of AI. A deeper inspection reveals a crowded trade, with eight stocks, including Microsoft, Google, and Meta, accounting for the majority of gains this year. Excluding these eight stocks, the market performance is relatively flat or slightly positive.

The Federal Reserve remains vigilant as the June possibility of another 0.25 basis point interest rate hike starts to gain traction, although it remains uncertain. It is worth reiterating that inflation is a challenging problem to tackle. While goods and housing inflation are easing, the unemployment rate below 4% continues to exert pressure on wages and services, making a swift return to 2% inflation unlikely. Additionally, inflation remains persistent in most developed countries, with even Japan defying expectations by recording inflation well above 3%.

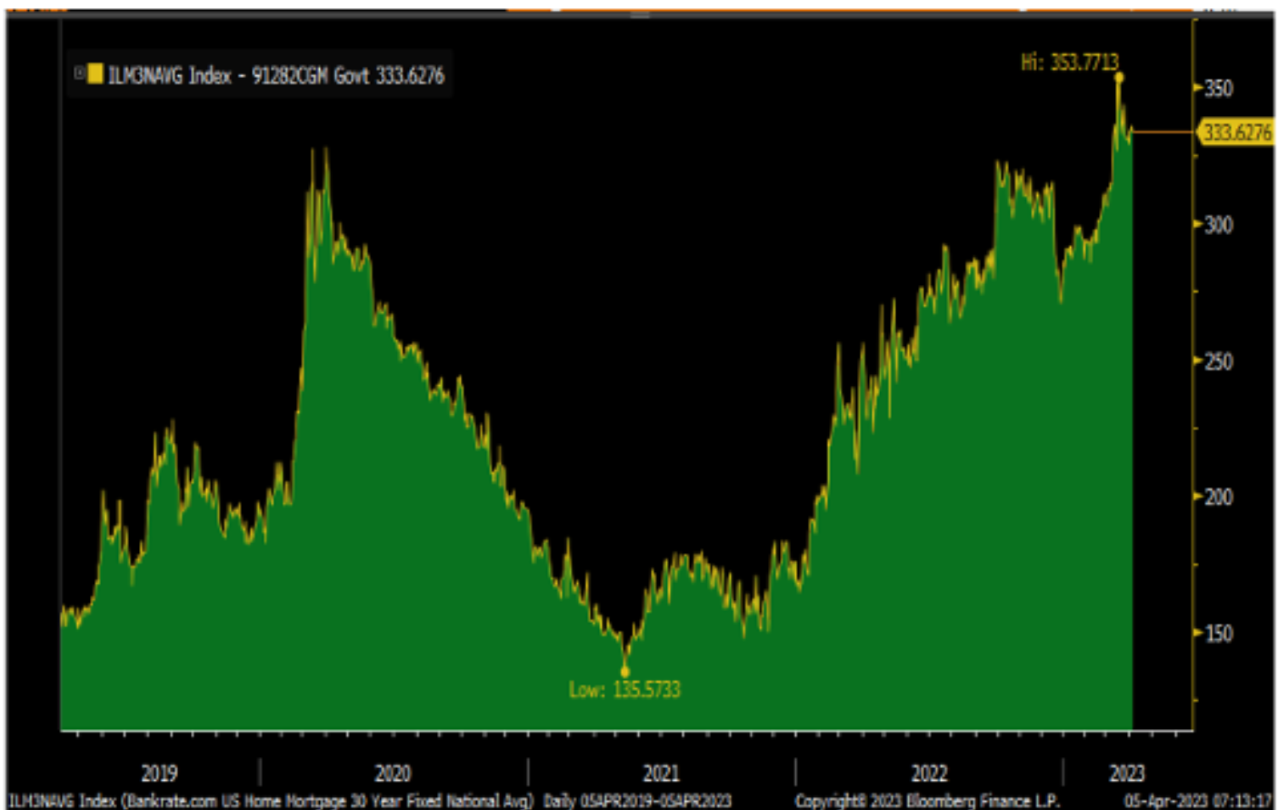

The Mortgage Maze

Quietly, interest rates have climbed back above 3.500% on the 10-year Treasury note. The future of rates will depend on how Congress addresses the debt ceiling and the potential for further flare-ups with regional banks. One thing is certain: obtaining financing for residential and commercial properties is becoming more challenging, requiring more expertise to navigate complex loan scenarios. Moreover, there is a significant divergence in rates among lenders, as illustrated by the discrepancy of 0.5% in the loan scenario priced today, emphasizing the value of a knowledgeable broker.

In this dynamic market environment, we remain committed to providing our clients with expert guidance and solutions to successfully navigate the ever-evolving lending landscape.